There were single college students, and couples in their 60's planning for retirement. A nice wide range of experiences. I loved hearing from the older couples. One man really took the envelope system to heart. He loves to go out to lunch with his buddies, and now does what he calls, "feelin' the cash." No longer is he mindlessly swiping his card at restaurants and unaware of how much he's actually spent. He told us that there are a few guys at his car dealership who make well over $100,000 and are up to their eyeballs in debt. They might have large incomes, but they are NOT wealthy.

I did a little research on my own. Dave calls the FICO score, an "I Love Debt" score because it basically measures how much debt you can get into. I looked up how they calculate your score, and this is what I found:

|

| From myfico.com |

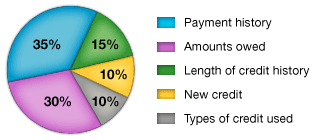

Ridiculous. Let's look at each section.

Payment history: if you've paid on time or not

Amounts owed: calculated by having a weird mix of not too much, but not too little debt either

Length of credit history: generally, the longer you've been in debt, the better

New credit: they just don't want you opening too many all at once.

Types: the score will consider your mix of credit cards, retail accounts, installment loans, finance company accounts and mortgage loans.

But! But! How will I ever buy a car or house without a credit score? The same way they used to before credits card even came to be. The old fashioned way!

The class was super fun. Dave is entertaining and explains things so well. This video is not from the actual class, but it's a nice little summary of what we learned.

No comments:

Post a Comment